No Interest Patient Financing: It Works

Susan Richardson

Vice President of Marketing

Unicorn Financial — Tallahassee, Florida

Over the last several years, practice management experts have identified some major patient financing trends that have helped successful dental practices substantially increase treatment plan acceptance. Your practice can and should benefit from these market friendly, no-interest patient financing plans. However, these plans can have pitfalls; therefore, it is important to openly communicate with your patients to avoid misunderstandings about patient financing payment plans.

The New Revolutionin Patient Financing

By far the most significant financing trend is the revolution brought about by no-interest financing, providing vivid proof that patients are also consumers. After its massive success in financing discretionary consumer products, no-interest financing has become the “gold standard” for financing dental services. One of the fastest growing patient financing companies reports that >80% of its customers choose no-interest financing. Additionally, dental practices that offer it to every patient can experience an increase of treatment plan acceptance by at least 10% to 25%.

Why the explosion in the market for this kind of attractive payment option? Simply because we all are consumers. For example, it is easy to imagine a consumer making a major purchase of $2,400 for furniture or, perhaps, a computer. What were the payment options? Write a check for $2,400? Put it on a credit card with 18% interest, which would tie up available credit? Clearly, the most attractive option is payment of $133.34 for 18 months, interest free. Similarly, faced with these same options it is almost certain that your patients will choose no-interest financing to ensure their dental health and attain that beautiful smile.

Convert Consults to Treatment Plan Acceptance

No-interest financing is especially helpful in increasing acceptance of larger, more comprehensive treatment plans which have higher fees. A longer repayment period of 18 or 24 months with no interest works exceptionally well with the comprehensive treatment plan fees because the patient is provided an additional 6 months of no interest to pay off the balance to the finance company. This is an option too attractive for credit savvy patients to not say ‘yes’ to treatment plans. The alternative is the possibility that, after an extensive diagnosis and consultation discussing fees, the patient leaves undecided—or worse yet—never to be heard from again.

In these cases, it is almost always the cost of treatment that caused the patient’s anxiety. The offer of no-interest financing can be a strong motivator to enable you and your staff to get a treatment plan commitment during consultation while the patient is still in your office.

There will always be patients who prefer, for one reason or another, traditional financing plans with the lowest possible payment. But hands down, no-interest payment plans have become the payment option of choice with today’s credit savvy consumers. To ensure the highest possible conversion rate, you should offer both extended and no-interest payment plans.

No Interest Plans: Equal Payments versus Low Monthly Payments with a Balloon

When selecting a patient financing company, be sure its no-interest programs are paid off in the months agreed to: 12-month programs in 12 months, 18-month programs in 18 months, etc. With some companies—although they may warn consumers in the fine print—the billing statement has only a small minimum monthly payment (usually 3% of the balance) with a large balloon payment at the end. This can frequently become an unpleasant surprise when interest from day 1 is assessed if the entire remaining balance is not paid off in the 12th month.

Therefore, it is imperative that your staff and your patients understand the differences between the no-interest plans with equal payments versus small minimum monthly payments with no interest for a fixed period followed by a balloon payment.

-

No Interest Plans that Pay Off with Equal Monthly Payments

- This equates to 12 equal payments for 12 months, 18 equal payments for 18 months, 24 equal payments for 24 months.

- The monthly payments are higher but patients avoid a large balance pay-off in month 12 and no interest is assessed.

- These plans are consumer friendly. There is no surprise balloon payment in month 12, and the balance is $0 if 12 payments were made on a timely basis.

- The balance is completely paid off within a short period of time so the patient or a household member can return for additional services, and future treatment is not delayed.

- Patients will not call your office complaining about not knowing about the balloon payment until month 12.

-

No Interest Plans with Small Monthly Minimum Payments and Large Balloon Payment

- There is a smaller minimum monthly payment printed on the statement (usually 3% of the balance) instead of 12 equal monthly payment amounts.

- A large balloon payment (88.7% of the amount financed) is due in month 12 because only 11.3% of the principal was paid.

- The patient may believe he or she has been tricked after paying only the 3% monthly minimum on the statement for the first 11 months.

- The interest is added from day 1 of the promotional period if the large remaining balance is not paid in full.

- The payment plan turns into a traditional extended payment plan with interest accruing every month.

- This plan may generate calls to your office by patients who believe your office misled them about repayment obligation when interest is tacked on from day 1 of the promotional period.

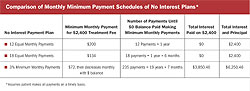

Example

Using a $2,400 example (see table), the minimum 3% monthly payment (at an interest rate of 22.98%) starts at $72 and decreases as the principal is paid down. If the patient makes 11 scheduled payments, the unpaid balance is still $2,128.60 or 88.7% of the original treatment fee. If the patient continues making the minimum monthly payment printed on the statement, he or she would have to make a total of 235 payments. Those payments translate into 19 years and 7 months to pay off the balance. Total payments would be $6,250.46 (260% more than the original treatment plan fee), with the total interest paid over the life of the amount owed being $3,850.46. The unfortunate result is your patient will be unlikely to be able to pay for future treatment because of the obligation to pay off the existing balance. If the patient feels taken advantage of, you risk losing the patient and any referrals the patient may have made to friends and relatives.

-

Avoiding Patient Financing Misunderstandings

- Initially, patients may be dazzled by the fact they can take advantage of a no-interest period. Ask your staff to communicate how your patient finance company’s no-interest plan truly works, including timely payment and penalties should the balance not be paid in full within the promotional period.

- If you are not offering a no-interest plan of 12 equal monthly minimum payments in 12 months (or 18 in 18 months, etc), be sure to inform the patient that paying the monthly minimum payment of 3% of the balance printed on the patient finance company’s statement will result in a large balloon payment in month 12. You will be surprised to know that many consumers generally pay only the monthly minimum amount on their statements and do not realize there will be a large balloon payment at the end.

- Do not rely solely on the patient finance company’s disclosures as the only communication about how the program works. Verbally disclose what penalties apply if the balance is not paid off on a timely basis within the promotional period. Some payment financing companies offer a payment options worksheet to assist your staff with explaining payments/ penalties.

- A happy patient or household member with his/her obligation paid off is likely to return for future dental services and refer friends and family to your practice. A disgruntled patient who feels he or she has been taken advantage of is unlikely to return to the practice or provide positive referrals.

- Be sure to contact your patient financing company to learn how your current no-interest plan works and consider changing companies if you do not like the answer. Also, establish training programs for your staff so they can clearly explain how the payment plans work.

Conclusion

In patient financing—whether for esthetic and general treatment plans, or to cover larger fees not covered by the patient’s dental insurance—your practice should offer no-interest financing. Your patients will benefit, and so will your practice. The 12-months, 18-months, and 24-months no-interest payment plans will very likely continue to be a preferred payment method. Now is a good time to learn how your plan works so that your patients can use this attractive option to pay for your services.

For more information, please contact the author at srichardson@unicornfinancial.com or call 1-888-388-7633.

|