You’ll Never Again Collect Your Full Fee (and Other Thoughts About Joining a PPO)

Jennifer Towers

You can spot preferred providers immediately in a crowd of dentists; they are the ones with the worried grins forever quoting their insurance adjustment figures. Alternately, their fee-for-service colleagues have the relaxed look of dentists who reliably can use their production numbers as a barometer for practice success.

It’s not the easy choice it seems to be. Considering whether or not to join a Preferred Provider Organization (PPO) is one of the most important decisions a dentist will make in his or her career. It’s safe to say that once someone embarks on the journey of claim filing and CDT coding, there’s no turning back.

Managed health care is now a way of life in the United States and dentistry is not an exempt field of medicine. Our industry is doing an excellent job of informing the public about the impact oral health has on their bodies, and we all have noticed the slow and steady paradigm shift of dentistry from simple pain-management to preventive and cosmetic care. The steady growth in concern over oral health is naturally paralleled by a growing public desire to make dentistry affordable. Goodbye, tooth loss. Hello, dental insurance.

Should dentists adopt the if-you-can’t-beat-them-join-them mentality when devising their practice policy on insurance? The answer to that question will only present itself after hours of research. This article is geared to get new and experienced dentists alike thinking about how insurance decisions can affect the landscape of their careers, from patient demographics and practice location to personal satisfaction and financial success.

WHAT ARE PPO PLANS?

As opposed to Capitation/Dental Maintenance Organization (DMO) plans, in which dentists accept regular, monthly bulk payments from insurance companies and then treat the patients sent to the practice by those companies, PPO plans are the more common form of network participation in the dental industry. Under a PPO plan, insured patients choose to seek care from a list of network dentists (ie, preferred providers) supplied by the insurance company. These dental providers bill their patients under the guidelines specified in a signed contract between themselves and the insurance company. The theories espoused by proponents of PPOs explain that participating doctors will benefit from the marketing capabilities of large insurance companies in ways that compensate for the reduced fees they agree to accept. In other words, in exchange for patient referrals, preferred providers consent to discount their work and join a network of colleagues who agreed to do the same.

HOW DO PPO PLANS WORK?

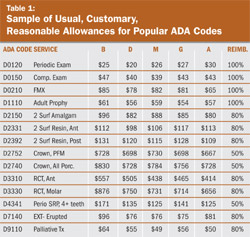

As contracted network dentists, they are bound to collect percentages of “usual, reasonable and customary fees” for each CDT code covered under the array of plans offered by any given insurance company. The companies determine these fees (also called allowable charges or fee allowances or fee schedules) by analyzing data including geographical spending trends, demographics, and provider fees. Employers then decide the percentage of coverage for each CDT code and formulate plans to offer their employees. Allowable charges are unrelated to the dentists’ actual service prices and often are significantly less than the practice fee schedule. For preferred providers, the difference between their fee and the allowable charge for approved procedures is subtracted from the patient balance. This is called an insurance adjustment or write-off. The adjustment can be significant in many cases and is applied to most of the procedures performed in a dental practice every day. Table 1 shows a sample of fee allowances for common dental codes. The data is indicative of figures for regions about 45 minutes outside of a major metropolitan area.

Every PPO dentist should pay close attention to this table and add a column for their practice fees for each CDT code. The difference between the practice fee and the allowable charge is an accounting loss for the dentist on a microeconomic level, and possibly on a macroeconomic level as well, once the yearly total of adjustments is calculated. The common thought among insurance companies, however, states that the dentist would not have the opportunity to perform that service for that particular patient if not for the fact that he/she was a participating provider. Therefore, in the eyes of the benefit-paying entities, it is not a loss of income but a gain for the preferred provider.

This lesson in semantics is one with which anyone thinking of joining a PPO should become acquainted. The probability of case acceptance is a difficult calculation and it becomes even more complicated when we factor in dental insurance. Perhaps the “income gain” mentality would be accurate if the patient was referred to the practice directly from the insurance company or if the patient would not have sought treatment from an out-of-network provider. In this author’s experience, it is often the latter that holds true rather than the former. In the author’s own practice, they have a .02% annual referral rate from insurance companies and have not calculated the retention of that patient pool. On the other hand, they have had 5% of patients leave the practice due to a change in insurance—their new plan was not one in which the practice’s providers were preferred.

In addition to allowable fees, insurance adjustments, and patient recruitment, there are other important factors to consider: annual insurance maximums, least expensive alternative treatment, preexisting conditions, and treatment exclusions. Each patient has a yearly maximum amount that the insurance company will contribute toward care. Many plans offer a $1,000 or $1,500 annual maximum which has been the average since dental insurance was created decades ago. Most patients are reluctant to enter into treatment once their maximum has been reached because they want to minimize their out-of-pocket expenses. It is important to note that, with many plans, the dentist still has to take the insurance adjustment even after the patient have reached their yearly maximum and the patients will have to pay for their portion plus the percentage typically paid by the insurance company.

Insurance companies typically stipulate that they will pay for the least expensive alternative treatment. The most common example of this practice is with posterior composites. Most insurance companies will only reimburse the dentist the amount allotted for a posterior amalgam restoration because it is less expensive for them to do so. There is a similar practice with posterior crown restorations; the insurance often pays the dentist for the cost of an all-metal crown rather than for a PFM. Insurance companies also have other ways of denying claims for treatment—many times they will not pay for fixed or removable prosthodontic work where the tooth or teeth were extracted before being covered under that particular plan. This is a called a “missing tooth clause,” which is a very common example of excluding coverage for preexisting conditions. Treatment exclusions are not atypical and some other examples are orthodontics, crown-and-bridge, implants, occlusal adjustments/ equilabration, veneers, and whitening. It is important to urge patients to to gain full awareness of their coverage in order to make informed treatment decisions.

WHO SHOULD BECOME A PREFERRED PROVIDER?

It stands to reason that dentists would not willingly discount their fees unless there was a demand to do so. Competition is the main reason any dentist should join a PPO. Patients base their dental decisions largely on price and comfort. If they are paying for insurance, they are going to use those benefits in a way that is effective for them. New dentists, clinicians moving or restarting practices, dentists in middle- or working-class locales, and providers in areas concentrated with dental practices should all consider what insurance companies and plans are acceptable additions to their businesses.

In some cases, dentists do not have to enter into the network in order to submit claims to a particular insurance company and get payments for their patients. Many insurance plans offer a lesser benefit for services performed by out-of-network providers and the patients are responsible for the difference between the service fee and the insurance payable amount. In this case, there is no insurance adjustment for the dentist. More established practices may find this type of insurance involvement suitable and this may facilitate patient acceptance if the eventual goal is to eliminate insurance entirely in a practice.

WHAT IF YOU HAVE TO TAKE INSURANCE?

As a preferred provider, you have little control over your fees when you are treating insured patients. Therefore, to stabilize the debit to collections suffered with your insured patients, you must raise your fees annually for two reasons: to subsidize your income loss through your fee-for-service, uninsured patients, and to be sure your fee profiles are updated as often as possible with the PPOs.

New dental school graduates and dentists moving their practices should do as much research as possible into the fee profiles associated with the possible locations/zip codes where the practice will be located. Once a clinician spends the time, money, and effort to establish a patient base in a certain area, it is difficult to move. Therefore, the insurance policy established by the practice at its onset will have lasting effects on its profitability. To PPO dentists, production is not the number by which financial success is calculated—collections are the key. Barring all other collections (difficulties such as bad debts and slow payers), preferred providers can expect to adjust approximately 30% of their annual production from insurance adjustments. That percentage fluctuates with experience in practice management and other factors.

If a dentist must accept insurance, he/she should be willing to pay for an attorney to review the contracts before they are signed, hire an educated, diligent practice manager or insurance administrator to become the practice expert on coding and reimbursement trends, and make peace with the fact that patients will tend to doubt the necessity of the treatment plan if services are not covered or are undercovered by their insurance plan.

Dentists must also understand that the types of insurance accepted by the practice have a determining role in the demographics of the patient base and in the forecasted profitability of the practice. It is not enough to look at the coverage for crowns, which is a common mistake. Approximately two thirds of most practices’ production is in services other than prosthetics and the preventive care codes are typically the most impacting.

If a PPO provider wants to reevaluate his/her insurance policy, it is important to start with data analysis. Contact each insurance company and ask for a practice summary report for the last 3 years. These summaries will provide information on the number of patients insured, amount submitted, amount adjusted, and amount paid. It may not be feasible to go fee-for-service completely but it may be worthwhile to revise the practice policies on accepting secondary insurance or to try and raise the fee profile for certain codes.

CONCLUSION

Accepting insurance is a way of life for over 80% of the general dentists and specialists in the United States. It is important for clinicians to educate themselves on the often-confusing details of insurance plans and how they function within the walls of a dental practice. Education will stave off frustration and confusion on the part of the dentist and patient and make for better practice management.

| |||||||

| Table 1 | |||||||

| |||||||